INDIAN ARMED FORCES CHIEFS ON

OUR RELENTLESS AND FOCUSED PUBLISHING EFFORTS

SP Guide Publications puts forth a well compiled articulation of issues, pursuits and accomplishments of the Indian Army, over the years

I am confident that SP Guide Publications would continue to inform, inspire and influence.

My compliments to SP Guide Publications for informative and credible reportage on contemporary aerospace issues over the past six decades.

Embraer – Expanding the Empire

With growing demand for regional aircraft, Embraer’s firm order backlog totalled $17.8 billion, reflecting an increase of 4.1 per cent from the last reported quarter.

From the first delivery of Embraer-Jet (E-Jet) to LOT Polish airlines in 2004, Embraer Commercial Jets has had significant global footprint. In October 2013, when India’s new low cost carrier Air Costa started operations with E-Jets, Embraer’s tally of aircraft deliveries globally had surpassed the magic figure of 1,000 jets with 61 customers in 43 countries. Indeed, an impressive story from the Brazilian aerospace major. In the Asia-Pacific region, Embraer commercial jets are making fast inroads as several operators are seeing the benefits of the Brazilian jets, none of which have the middle seat.

China leads with three operators – Tianjin Airlines, China Southern and Hebei Airlines – making the best of the E-Jets. Japan (J-Air and Fuji Dream Air) and Australia (Virgin Australia and Airnorth) have two operators each and there is a growing interest in the region, considering Embraer has been talking about the ‘right-size’ to capture untapped markets.

Power of 70-120 Seat Segment

Embraer has been banking upon a few entrepreneurial carriers who have recognized the power of the 70 to 120 seat aircraft capacity segment. These airlines with their fleets of E-Jets have brought affordable, quality air service to secondary markets not just in Brazil but in other countries where the aircraft flies. Carriers in Africa, China and Central Asia are all discovering the enormous potential of the 70-120 seat aircraft to build network connectivity with lower-risk increments of seat capacity.

In its market outlook 2012-2031, Embraer has indicated that the centre of gravity for aviation will move eastward, most notably to Asia and, to some extent, southward to Latin America. The main drivers that will impact the global air travel industry include – strong pace of economic growth in emerging markets; economic growth driven by middleweight cities and surge of an urban middle class. Embraer has forecast that world air transport demand will increase roughly 2.7 times by 2031, reaching 13 trillion Revenue Per Kilometre (RPK). By 2031, Asia-Pacific and China will be the largest market in the world, accounting for 34 per cent of world’s RPKs. Europe and North America will follow at 21 per cent RPKs each.

World Demand

With such growth potential, Embraer has forecast that there would be world demand for 6,795 new jets in the 30 to 120 seat capacity segment over the next 20 years, representing a total market value of $315 billion.

The 90 to 120 seat segment will be the largest market with 3,765 new deliveries in the next 20 years, representing 55 per cent of the segment, followed by the 61 to 90 seat segment with 2,625 new deliveries or 39 per cent and the 30 to 60 seat segment with 405 new deliveries or six per cent.

Asia-Pacific’s economic outlook is above average with an annual GDP growth rate of 3.4 per cent forecast for the next 20 years. Japan and India will be at the forefront, followed by economies of Australia, Indonesia, Malaysia, the Philippines, South Korea, Thailand, Taiwan and Vietnam. Growing trade links between countries within the region will not only promote local economic prosperity but also drive the need for improved air transportation links.

LCCs to Boost Air Connectivity

Low Cost Carriers in Asia-Pacific will continue to be one of the primary engines of market liberalisation and growth in the region. Such growth will be largely pursued in trunk markets with increased competition. As markets become more liberalised and trunk markets mature, airlines will require 61 to 120 seat aircraft to optimally serve these markets. The Asia Pacific market consists mostly of secondary markets with low and medium demand densities (20 to 300 passengers Per Day Each Way – PDEW). Over half of the flights below 3,500 km in Asia Pacific take off with fewer than 120 passengers onboard, whereas 67 per cent of the singleaisle aircraft flying today have over 120 seats. The majority of secondary markets have medium-haul distance profiles that are better suited for up to 120 seat jets than turboprops.

Embraer states that 35 per cent of secondary markets in Asia Pacific are not served non-stop, and more than half of all markets served do not allow for same day (return) travel. Since bilateral restrictions limit service improvement to secondary markets and higher density trunk markets are still growing at attractive rates, airlines in Asia Pacific are not optimised to serve low and medium-density routes. Secondary markets will experience faster growth rates than trunk markets. Therefore, some of these secondary markets will grow to be dense enough to sustain optimised service by narrow body equipment. Nevertheless, at forecasted growth rates, the majority of Asia Pacific markets will still be in the medium-density range (between 50 and 300 PDEW).

Embraer forecasts a need for 505 new aircraft in the Asia Pacific region during the next 20 years, 64 per cent of these units to support growth and 36 per cent to replace older generation aircraft. The 30 to 120-seat jet fleet will increase from 185 units in 2011 to 505 by 2031.

China Connecting Hinterland

China is a key market and the aerospace majors are positioning themselves to capture this market. Presently, the Chinese government is hoping to stimulate traffic to less developed regions in the central and western regions thus opening up the aviation sector further. Jets with fewer than 120 seats account for only nine per cent of the Chinese single-aisle fleet, which is insufficient for regional operations. In comparison, in the US the percentage is about 30.

Opportunities abound as three quarters of Chinese domestic market consists mostly of low and medium density demand between 20 and 300 PDEW which are best served by aircraft lower than 120 seats. Embraer forecasts a need for 1,005 new aircraft in China during the next 20 years. Considering these trends, Embraer is positioning itself well globally to address the growing demand. It is quite a competition for aerospace majors in each of the seat segments – 30 to 60 seat capacity; 61 to 90 and 91 to 120.

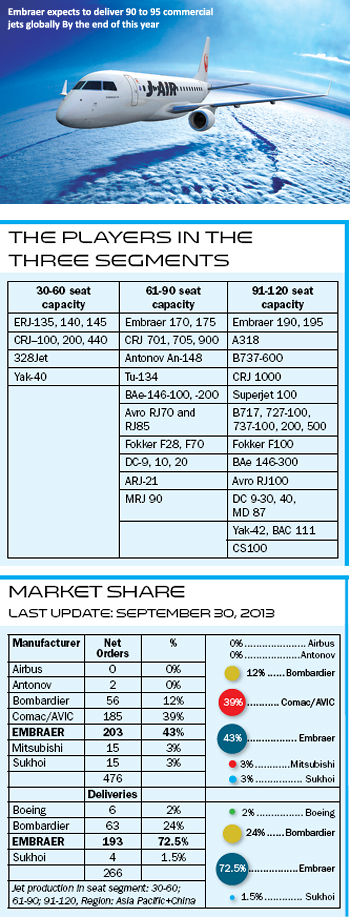

The Embraer family of jets has been strategically placed in the 30 to 120 seat segments and the marketing has been aggressive. The accumulated net orders for Embraer as of September 2013 for Asia-Pacific plus China region were 203 and the accumulated net deliveries were 193. In terms of deliveries the nearest competitor was Bombardier with a figure of 63 while the accumulated net orders were 185 of the nearest competitor – Comac. By the end of this year, Embraer expects to deliver 90 to 95 commercial jets globally for which the company has been aggressive in its marketing. The company expects to achieve total net revenues between $5.9 billion and $6.4 billion with commercial aviation contribution being as high as 52 per cent, followed by executive aviation at 25 per cent; defence and security at 21 per cent and other business at two per cent. The total 2013 Investment is expected to be $580 million, of which research will represent $100 million, product development $300 million and CAPEX $180 million. With growing demand for regional aircraft, Embraer’s firm order backlog totalled $17.8 billion, reflecting an increase of 4.1 per cent from the last reported quarter. This marked a four-year high in the company’s backlog history. In terms of aircraft breakdown, Embraer’s order backlog comprises 140 E-175; 100 E-175-E2; 78 E-190; 25 E-195-E2; 22 E-195 and 6 E-170 jets.

Not for nothing, is Embraer the world’s third largest commercial aircraft manufacturer after Boeing and Airbus.

SP's Aviation - Current Issue