BizJets Holding the Fort

The repercussions for the global economy from the Ukraine invasion appeared to be small in terms of immediate reduction in flight activity: WingXAdvance

For over a month now, the global headlines have been dominated by Russia’s invasion of Ukraine. During the initial stages of the invasion, for business aviation, the Ukraine crisis was having a direct effect on a relatively small share of overall flight activity, but the proliferation of sanctions was expected to significantly complicate the whole business aviation market, especially in Europe, across the field from flight operations to charter brokerage, aircraft financing, management and maintenance. This was noted by the global business aviation market analysis firm, WingX Advance.

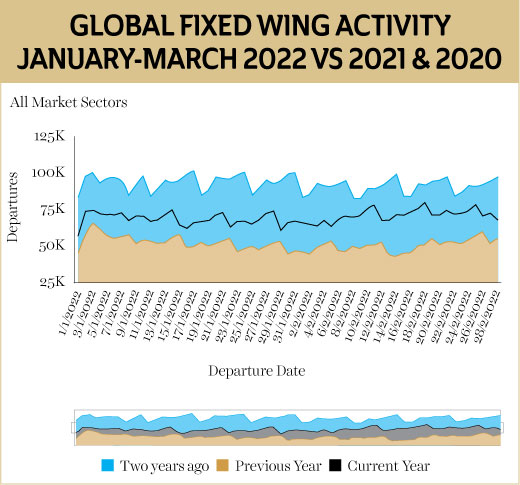

The global trend in business jet activity had not really registered any impact from the Ukraine crisis up until the beginning of March. The 2022 trend, since the start of the year, indicated a 13 per cent increase over comparable 2019, with scheduled airline sectors still lagging by 31 per cent, despite a 38 per cent bounce so far this year. However, nearing the mid of March as the crisis continued to escalate, the industry was looking with trepidation at the repercussions for the global economy from the Ukraine invasion. The effect, however, appeared to be small in terms of immediate reduction in flight activity as was noted by WingX Advance. The swift decline in outbound flights from the directly affected regions was more than offset by the ongoing strong demand for on-demand travel as the final constraints on travel restrictions are lifted in Europe and the US.

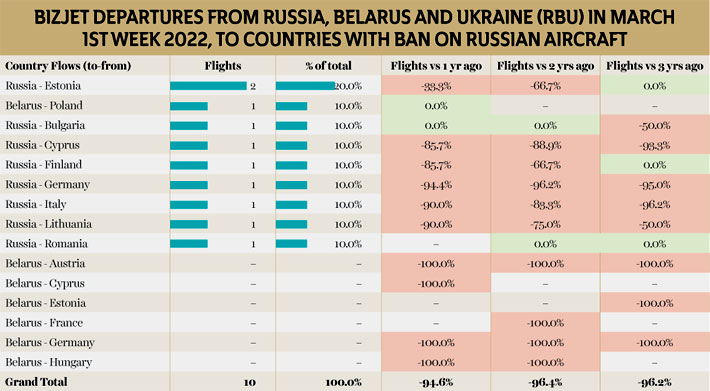

In the beginning of March, significant consequences emerged for the global aviation industry owing to the Russia-Ukraine situation. In terms of flight activity, Russia, Belarus and Ukraine (RBU) witnessed precipitous drops in all flight activity over the last few days. However, the declines in flight activity out of RBU accelerated sharply during the second week of the invasion. Compared to activity in the previous week, scheduled passenger airline sectors were down 54 per cent, cargo flights down 66 per cent, business jet departures down by 57 per cent. Compared to the same first week of March in 2019, business jet departures from these three countries were down by 39 per cent. To put this in context, WingX added that up until the invasion, business jet departures from Russia were up by 25 per cent compared to the January-February period of 2019. The biggest declines, unsurprisingly, have been to those countries which have implemented airspace bans on Russian-controlled aircraft. In business jet activity, Charter and Aircraft Management operators are seeing the largest activity declines in the region.

John Tuten, Chief Pilot for Honeywell and Chair of the NBAA International Operations Committee, noted during an NBAA News Hour that the closure of Russian airspace has impacted roughly half of all routes between the US to India and the Asia-Pacific. “In some instances it’s adding five hours of flight time” to divert around the closures, he said.

Relatively, Russia domestic activity is more resilient, representing almost half of all bizjet flights, and 10 per cent higher than the same week back in 2019, noted WingX’s report. It further added that:

- The busiest bizjet city pairs include St Petersburg, Kazan and Moscow.

- For domestic trips, the Falcon 900 emerged as the busiest business jet in the second week of March.

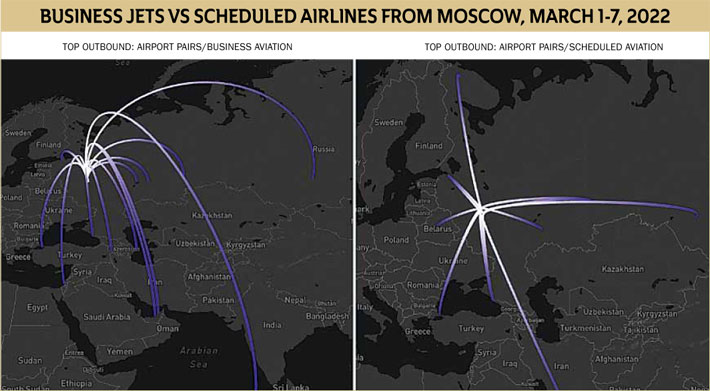

- Flying international, the most popular destination is UAE, and specifically Dubai. With 49 outbound flights in the first week of March, the Russia-UAE connection was three times busier than pre-pandemic, but just two thirds of the outbound activity during the last week of February.

- The Embraer Legacy 600 accounted for more than 60 per cent of these trips.

- Next most popular international destinations were Baku and Istanbul.

SIZE OF THE RUSSIAN AVIATION

In the beginning of March, the report also brought into notice, the size of the Russian aviation industry in the global context. The size was noted to be small in some respects. For instance, only 0.5 per cent of global business jet deliveries, 0.7 per cent of the active fleet, under 100 aircraft on the register. However, Europe has relatively high exposure to business jets regularly operating out of Russia, an estimated 12 per cent of all jets based in Europe in 2021. Last year, seven per cent of all business jet sectors operated in Europe interconnected with Russia or Ukraine, 12 per cent of Gulfstream jet movements in Europe, 28 per cent of Embraer Legacy 600 sectors. 12 per cent of globally active ultra-long-range jets had at least one movement in Russia during 2021. Over the last two days though, business jet connections between Russia and the Middle East have grown much faster than European connections. This is reflected in the last few days’ departures from Moscow airports.

The North American market was underlined as much less exposed than Europe to direct flight connections with Russia in the beginning of March. Although overflight restrictions are now in force, and the leading US suppliers of business aviation services will be severely constrained in supporting Russian aviation concerns since widespread sanctions were implemented, added WingX.

Among the latest sanctions from the industry, Canadian airframer, Bombardier “has suspended all activities with Russian clients, including all forms of technical assistance. As a company with deep roots in communities around the world, we are first and foremost concerned with the loss of human life and the toll this conflict is taking on families. We will do our part, in any way possible, to help the governments of the world pursue an end to this horrific conflict,” the OEM said in a statement released on March 11, 2022.

Within the US, the pattern of business jet demand is familiar, with Florida the primary hub, California and Texas back above 2019 levels, and the North-East slower to recover; New Jersey, and Teterboro in particular, are still behind 2019 activity volumes. Overall, he biggest rebound this year in the US market has been in the ultralong-range jets, sector is 24 per cent above pre-pandemic records. Private flight departments are belatedly recovering.

Although not a large petroleum provider to the US, sanctions against Russian oil shipments to other countries will also carry significant consequences to the global market. “Our economists have started modeling scenarios [at] $150 a barrel,” said David Granson with Goldman, Sachs & Co. at NBAA News hour, due to anticipated international supply chain shocks, coupled with high demand as travel returns to pre-pandemic levels.

Ron Epstein, Senior Equity Analyst for Bank of America, said he expected other supply chain shortages as well, particularly as Russia is among the largest global suppliers of titanium and other materials used in aircraft production. “If you’re doing business with these folks, you have to be really careful given how the sanction environment is changing, quite literally, almost by the hour,” he said.

EUROPE

Going by the WingX data at the time of this report, business jet activity in Europe continued to exceed pre-pandemic levels despite the Ukraine crisis. In the first week of March, bizjet sectors were up 17 per cent compared to March 2019, and as a mark of the recovery from Covid restrictions, fully 50 per cent more activity than comparable March 2021. Strong bizjet demand in Europe also reflects the ailing scheduled network, trending 30 per cent below pre-pandemic levels so far this year. Demand for fractional and charter flights has provided momentum for the last 6 months, although the most recent boost has come from recovering non-commercial flight departments, including corporate flight departments.

NORTH AMERICA

The North American market is evidently insulated from the immediate effects of the Ukraine crisis, and is seeing the “tail end” of the recover from Covid, with most benefit for the largest cabin aircraft flying multiple-hour sectors. For example, ultra-long range jet activity is up by 28 per cent. In the largest cabin aircraft, the bizliners, the Airbus ACJ is rapidly recovering on pre-2020 activity, although notable BBJ fleet activity is trailing, sectors 60 per cent below where they were in March 2019. The lighter end of the fleet has been the biggest beneficiary of the recovery, with Cessna’s North American fleet flying 35 per cent more sectors this March compared to 2019.

REST OF WORLD

The regions outside of North America and Europe, including Russia, have seen the strongest of all rebounds in bizjet flights in 2022, with a 52 per cent increase in this March compared to three years ago. Brazil, Argentina, Australia, India, Nigeria, have all seen much higher activity than pre-pandemic. There are a few countries which haven’t seen such a strong recovery and these are mainly in Asia. In this region, prolonged pandemic restrictions and turbulent geopolitics have constrained flight activity, particularly flight hours. China has seen the biggest slowdown, with outbound sectors down by 48 per cent in the first week of this month compared to 2019.

EXPERTS EXPRESS

The ways in which the hostilities between Russia and Ukraine have impacted the global business aviation community, and likely ramifications as the crisis evolves, were the topics of discussion during an NBAA News Hour webinar where experts from across the industry gathered to deliberate.

International sanctions against Russia also will affect aircraft transactions. “If you buy an aircraft that was owned by a blocked entity, the government’s going to seize it and start a forfeiture procedure. You better have documented that you did [your due] diligence and were a buyer in good faith,” advised Jonathan Epstein, partner at Holland & Knight LLP.

There was also a hint towards cyber concerns during the discussion. Cyber-attacks against Ukraine and members of the North Atlantic Treaty Organisation (NATO), including the US, also are likely. Fuel prices; longer routes; delayed timelines; bans, fear of uncertainty is also expected to play role as the situation emerges. Despite these challenges, financial analysts are generally positive about the global economy and the business aviation market. To put in Ron Epstein’s words, “We’re still bullish on business aviation. Ultimately, the Russian economy is about the size of Spain. It’s a player, but it’s not like China.”

Agreeing with Epstein’s sentiments, Granson added, “We’re very constructive on growth around the world. It’s a scary time, but we do believe we’re going to finish the year better than where we started from a business perspective and economic perspective.”

BizAvIndia - CURRENT ISSUE